Euro downside risks are still dominated by the sovereign debt crisis and potential oil supply shocks, says Todd Elmer, currency strategist at Citi.

Monday, February 28, 2011

Midday Currency Wrap for Monday February 28, 2011

Dove Versus Hawks - That's what this week's trading in the forex market will come down to. The Dove, represented by the US Federal Reserve, will stress that higher oil prices are a negative to growth and will likely signal continued support for the central bank's quantitative easing program. Federal Reserve Chairman Ben Bernanke testifies to Congress on Tuesday and Wednesday and he is expected to stick to his recent economic assessment that the recovery is strengthening but still not enough to bring about a significant improvement in the jobs market. The Hawks, represented by the rest of the world, will stress that higher oil prices will push inflation higher which will need to be tackled with increases in interest rates. European Central Bank President Jean-Claude Trichet may indicate this week that he is ready to increase borrowing costs. In fact, euro zone inflation data for January came in at 2.3% year-on-year, slightly softer than was expected but hovering at a 27-month high. The caused the Euro to move past 1.3840 level in early trading but the Euro has since come off as political elections in Ireland and Germany had a decisive no bail out undertone to them. The ECB, which has kept its key interest rate at 1% since May 2009, will hold its next policy meeting on March 3. Also representing the hawks, Riksbank Governor Stefan Ingves, who said that the central bank may boost interest rates at every meeting this year. In Canada, the CAD hit its highest level in three years after a report showed the nation’s economy grew at a better than expected 3.3% annual pace in Q4. Today's report has backed Bank of Canada Governor Mark Carney into a corner - growth is picking up but the currency's strength may stall growth. No change in monetary policy is expected at tomorrow’s meeting of the Bank of Canada, but expectations will change according to Carney's comments.

Sunday, February 27, 2011

Ireland vs The EU; The Gloves Come Off

As the people of Ireland went to the polls on Friday, the EU, through a Brussels spokesman, took the opportunity to remind the Irish public who their boss was. Here a sprinkling of what the EU declared:

The EU-IMF bailout "must be applied" whatever the will of Ireland's people or regardless of any change of government.

"It's an agreement between the EU and the Republic of Ireland, it's not an agreement between an institution and a particular government."

"The more the Irish make a big deal about renegotiation in public, the more attitudes will harden."

"It is not even take it or leave it. It's done. Ireland's only role in this now is to implement the programme agreed with the EU, IMF and European Central Bank. Irish voters are not a party in this process, whatever they have been told."

Them are fighting words. The EU will probably agree to renegotiate the interest rate on the bailout but they will not agree to giving haircuts to bondholders because the bondholders are banks in the UK, Germany, France, and Belgium; and if they have to right down the value of bonds then they may need bailouts as well. The Irish are looking for a referendum on the issue, but the EU doesn't want them to go down that road.

Well the Irish made statements of their own, the best one coming from Declan Ganley, the Irish businessman who led the 2008 No vote to the Lisbon Treaty. Ganley said: "Ireland must have the balls to threaten debt default and withdrawal from the single currency. We have a hostage, it is called the euro. The euro is insolvent. The only question is whether Ireland should be sacrificed to keep the Ponzi scheme going. We have to have a Plan B to the misnamed bailout, which is to go back to the Irish Punt."

Stay tuned this is going to be a great fight, read more here.

Saturday, February 26, 2011

The Week Ahead by MarketWatch Videos

Asia's Week Ahead: India's Budget, RBA

Feb. 25, 2011

Federal budget from India, manufacturing indicators from China and interest rate decisions from Australia and Indonesia will take the spotlight this coming week in Asia. MarketWatch's Phani Kumar reports.

Europe's Week Ahead: Bayer, HSBC and Carrefour

Feb. 25, 2011

Bayer, HSBC and Carrefour to report earnings next week. European Central Bank decision expected Thursday and may be accompanied with a change of tone on inflation.

U.S. Week Ahead: Jobs, Fed and Payrolls

Feb. 25, 2011

The coming week will end with critical data on payrolls and unemployment. Before that, Fed Chairman Ben Bernanke will appear twice before Congress to deliver his monetary-policy report. Greg Morcroft reports.

Feb. 25, 2011

Federal budget from India, manufacturing indicators from China and interest rate decisions from Australia and Indonesia will take the spotlight this coming week in Asia. MarketWatch's Phani Kumar reports.

Europe's Week Ahead: Bayer, HSBC and Carrefour

Feb. 25, 2011

Bayer, HSBC and Carrefour to report earnings next week. European Central Bank decision expected Thursday and may be accompanied with a change of tone on inflation.

U.S. Week Ahead: Jobs, Fed and Payrolls

Feb. 25, 2011

The coming week will end with critical data on payrolls and unemployment. Before that, Fed Chairman Ben Bernanke will appear twice before Congress to deliver his monetary-policy report. Greg Morcroft reports.

Friday, February 25, 2011

U.K. Faces Stagflation

Weak growth and high inflation have raised the ugly prospect of stagflation for the U.K. economy. The Bank of England's likely response will be to raise rates, but so slowly that they're unlikely to have much of an impact on growth or inflation.

Morning Currency Wrap for Friday February 25, 2011

Position Squaring Ahead Of Big Week - The GBP finish off the week with the poorest showing of all the majors, capped off today with downward revision to Q4 GDP to -0.6% from -0.5%. Now the question in the market will be how can any MPC member vote in favor of a rate hike with these numbers. Next week there are central bank meeting for the ECB and the Bank of England so we will probably hear more inflation-fighting rhetoric. For the Euro, today's election results in Ireland will be watched for any anti Euro rhetoric. Meanwhile, the Yen, CHF, and gold came off there weekly highs as price of oil eased allowing stock markets to eke out some gains. Take this as a breather rather than a change in trend as the unrest in North Africa and the Middle East show no sign of abating. In the US, the main focus next week will be the jobs reports and Federal Reserve Chairman Ben Bernanke is scheduled to deliver his semi-annual report on monetary policy to the U.S. House of Representatives' financial services committee on March 3. The jobs report needs to bounce back from its recent weakness and the market will try to gleam any new insight into possible end of QE2 or worse the possibility of a QE3. In Canada, the CAD pushed to a 3-year high in overnight trading but back off this morning as the price of oil came off a little and the US GDP report disappointed the market. U.S. economy expanded at an annualized rate of 2.8% in Q4, which was down from the advance reading showed growth of 3.2% and the expected reading of 3.3%.

Thursday, February 24, 2011

Pimco's Mohamed El-Erian on Bloomberg Television

Mohamed El-Erian, CEO and co-CIO of Pimco, appeared on Bloomberg Television's "Surveillance Midday" with Tom Keene this afternoon to discuss the unrest in the Middle East.

Morning Currency Wrap for Thursday February 24, 2011

Safe-Haven Flows & Interest Rate Expectations - All you need to know about the forex market right now is that the two main drivers are safe-haven flows and interest rate expectations. Safe-haven flows are going into the Yen, CHF, and gold as the ongoing political turmoil in the Arab world continues. What is utterly shocking here is that the USD is not picking up any safe-haven flows to speak of, times are a changing. Meanwhile, the GBP and Euro are being well bid as the market continues to price interest rate increases sooner rather than later while US interest rates continue to stay near zero. In Canada, the CAD started its long anticipated move up against the USD as prices extended gains on turmoil in Libya. Brent crude reached $120 per barrel today and since Canada is a net oil exporter the CAD pushed higher. Let's not forget the CAD has two nick names the "loonie" and the "petro dollar" and the latter is asserting itself in this market.

Wednesday, February 23, 2011

No Safe-Haven Flows for the USD

The U.S. dollar hasn't seen traditional gains as investors seek safer vehicles for shielding money from turmoil in the Middle East and North Africa.

Afternoon Currency Wrap for Wednesday February 23, 2011

Arab World Unrest & Rising Interest Rate Expectations - The combination of continued unrest in the Arab world with rising expectations of interest rates increases virtually everywhere in the world except the US has weighed on the USD today. The USD is not seeing the safe-haven flows due to the unrest that it is usually accustomed to seeing, mainly because of its negative fiscal and monetary policies. Add to this, rising interest rate expectations in Europe and the UK and you get a USD that is on its back foot. In Europe, ECB officials Yves Mersch and Nout Wellink said today that they were ready to fight inflation by raising rates when needed, prompting rate futures to price in a 25 basis point hike in August. This comes after last week's warning by Italian central bank governor Mario Draghi. ECB President Jean-Claude Trichet is due to speak today, so we will be looking to see whether he adds to the hawkish tone of other ECB members. Also putting a floor under the Euro was a signal from German Chancellor Angela Merkel that she would consider to renegotiate the terms of Greece’s bailout. In the UK, the GBP jumped after minutes to the February policy meeting showed a third policymaker voted for a rise while others would consider one if UK economic recovery resumed. But the real surprise was that BOE's head economist Dale voted with Sentance and Weale in favor of a hike and not the Deputy Governor Bean, who last week declared that he had joined the hawks. So now the market will speculate that Bean that will join the rest of the hawks at next month's meeting, setting the stage for a May rate hike. In Asia, the USD reach its lowest level in almost 2 weeks against the Yen even though Japan surprised the market with its first trade deficit in almost two years in January. In Canada, in a head scratcher the CAD lost ground during the morning trading succession even though the price of oil pushed past $100 a barrel.

Tuesday, February 22, 2011

Experts Shine Light on World's Currencies

WSJ's David Wessel sits down with three senior experts in international finance - Edwin M. Truman, Joseph E. Gagnon and Eswar Prasad - for a discussion on the major issues facing currencies and the global economy. I must warn you that these guys our economist and not traders, which means that if you take investment advise from them you will be assured to loss money.

Morning Currency Wrap for Tuesday February 22, 2011

Violence In Libya, Earthquake In New Zealand = Volatility - Here we go again, the CHF, Yen, and gold rose across the board amid speculation unrest will keep spreading in North Africa and the Middle East as violence in Libya boosted demand for the safest assets. The Libyan government attacked protesters and rebels claimed control of the second-biggest city, Benghazi, according to Al Jazeera television. What has been particularly unusual is the utter lack of safe-haven demand for the USD. Yes the North American market was closed yesterday so that would partly explain this, but today's flow into the USD is not would it would usually be - this is an ominous sign for the USD. Meanwhile, the Euro was able to shrug its earlier losses after European Central Bank council member Yves Mersch hinted that the ECB may adopt a tightening bias. “I would not be surprised at most colleagues concluding that we have upside risks to price stability,” Mersch said in an interview in Luxembourg yesterday. With the economy strengthening and inflation in breach of the ECB’s 2% limit, policy makers will “inevitably” have to “rebalance our monetary policy stance,” Mersch said. The ECB is scheduled to hold its next policy meeting on March 3. In Asia, the Yen managed to shake off its latest tussle with a credit rating agency and move higher. Moody’s Investors Service changed its outlook on the government’s credit rating to negative from stable. Meanwhile in New Zealand, the NZD was down by about 2% after an earthquake measuring 6.3 on the Richter scale struck the nation’s second- largest city, Christchurch, killing at least 65 people, as the market removed the likelihood of a previously discounted rate hike. In Canada, the CAD was slightly off after the retail sales report for December showed that sales fell 0.2% from the year-earlier. However, as I discussed in my blog yesterday, it is just a matter of time before the CAD de-couples from the USD and follows the price of oil and gold higher due to the ongoing turmoil developing in North Africa and the Middle East. Oil prices surged $6.50 to $92.70 and gold prices rose $12.61 to $1,401.20 per ounce in early trading today.

Monday, February 21, 2011

Oil Shock, Is the CAD about to Orbit?

The spectre of full civil war in oil-rich Libya has moved the North Africa - Middle East crisis into a more dangerous phase, setting up the potential for an explosive oil shock that will be much worse than the 1970's oil crisis. US oil contracts jumped to over $94 and Brent crude traded as high as $108 today. From a forex perspective, what has been particularly unusual is the utter lack of safe-haven demand for the USD, that has instead gone to the CHF and gold. With North American markets closed today for public holidays, I think we will begin to see the CAD unshackle itself from the tight trading range that it has been in and begin to push past recent 3-year highs.

Euroview: Are Republicans Undermining Dollar?

With the House of Representatives deciding over the weekend that Federal budget cuts are needed, the dollar may decline if it's perceived that the cuts are a danger to US economic recovery.

Sunday, February 20, 2011

Merkel's Party Suffers Defeat in Hamburg , is the Euro at Risk?

G20 Meeting; Another Photo Opp Or Real Results?

Interestingly, upon rereading the communiqué, I see that it wasn't just targeted to China but also the US. In paragraph 3 of the communiqué, subsection (i) (public debt and fiscal deficits) is targeted to the Americans while subsection (ii) (the external imbalance composed of the trade balance and net investment income flows and transfers) is target towards China. In other words, the rest of the world has had enough of China's unfair currency policy and America's irresponsible fiscal and monetary policy.

The Week Ahead by MarketWatch Videos

Asia's Week Ahead: Thailand, Hong Kong Data

Feb. 18, 2011

Next week, Thailand will release its fourth-quarter gross domestic product data, Hong Kong is set to report a budget surplus for the current fiscal year, and we'll see the latest report on Japan's core consumer prices. MarketWatch's Lisa Twaronite reports.

Europe Week Ahead: Ireland election, bank earnings

Feb. 18, 2011

Voters in Ireland will go to the polls on Friday in a closely watched election. Meanwhile, Commerzbank, Royal Bank of Scotland Group and Lloyds Banking Group will all report earnings next week.

U.S. week ahead: Mideast trouble watch continues

Feb. 18, 2011

Protests across the troubled region will continue to affect U.S. markets and could push oil and gold prices higher during a holiday-shortened week. Housing and GDP reports also are due. MarketWatch's Greg Morcroft reports.

Feb. 18, 2011

Next week, Thailand will release its fourth-quarter gross domestic product data, Hong Kong is set to report a budget surplus for the current fiscal year, and we'll see the latest report on Japan's core consumer prices. MarketWatch's Lisa Twaronite reports.

Europe Week Ahead: Ireland election, bank earnings

Feb. 18, 2011

Voters in Ireland will go to the polls on Friday in a closely watched election. Meanwhile, Commerzbank, Royal Bank of Scotland Group and Lloyds Banking Group will all report earnings next week.

U.S. week ahead: Mideast trouble watch continues

Feb. 18, 2011

Protests across the troubled region will continue to affect U.S. markets and could push oil and gold prices higher during a holiday-shortened week. Housing and GDP reports also are due. MarketWatch's Greg Morcroft reports.

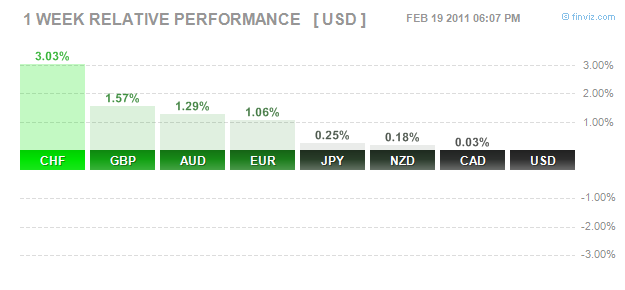

Saturday, February 19, 2011

Friday, February 18, 2011

Forex: Risk On, Risk Off Could Soon Be History

Portugal Bailout Looks Likely

Inside the News: Portugal Bailout Looks Likely: CMC's Hewson, Thomson Reuters: Reuters Insider

http://insider.thomsonreuters.com/link.html?cn=share&ctype=group_channel&chid=3&cid=192725&shareToken=MzpjMmZhYTNkYi1iYTgwLTQ0NjQtYjViMS05OGYyZTI5MjBiMTk%3D&start=0&end=252

http://insider.thomsonreuters.com/link.html?cn=share&ctype=group_channel&chid=3&cid=192725&shareToken=MzpjMmZhYTNkYi1iYTgwLTQ0NjQtYjViMS05OGYyZTI5MjBiMTk%3D&start=0&end=252

Morning Currency Wrap for Friday February 18, 2011

Isn't It Ironic - I could start this commentary just like I did yesterday, in fact I think I will because the safe haven flows are still intact and the only thing that changed was the Euro and a policy change in China. The CHF, Yen, and gold rose across the board amid speculation unrest will keep spreading in North Africa and the Middle East as protests continued in Bahrain, Libya, Yemen and Iran, boosting demand for the safest assets. The Euro spiked lower in early trading but later regained its losses and moved higher after a Bloomberg report quoting European Central Bank official Lorenzo Bini Smaghi saying the central bank may tighten policy as price pressures mount. It sounds to me like Smaghi is auditioning to become the next ECB president by appealing to Germany. The reason the Euro spiked lower was due to fear about a spike higher in emergency overnight borrowing from the ECB. It looks like a European bank was willing to pay high rates in order to get the funding reinforcing worries about financial stress within the euro zone and a bank getting in trouble. Portuguese bond yields continue to hover above the 7% level which was the level that caused Greece and Ireland to seek a bailout. In the UK, the GBP reached a two-week high against the USD after UK retail sales surged last month by almost four times the amount that was expected, suggesting that the Bank of England may have to raise rates. In Asia, the AUD briefly dipped lower after China's central bank raised its bank reserve requirement for the second time this year, following up on an interest rate rise earlier this month as it tries to combat inflation. However, the AUD recoup all of its losses later as the market realized that China effectively took its foot off the accelerator with the hike in bank reserve ratio requirements instead of putting its foot on the brakes, which would be akin to hiking lending and borrowing rates. In Canada, the CAD moved off yesterday's levels after data that showed Canada's annual inflation rate eased, suggesting that the Bank of Canada was under no immediate pressure to hike interest rates sooner than expected. The central bank makes its next announcement on interest rates on March 1. Canada's annual inflation rate slipped to 2.3% in January from 2.4% in December as energy price increases eased. Isn't it ironic that yesterday's inflation rate in the US rose more than was expected but the US Fed has no intention of hiking rates while in Canada the inflation rate eased but the market still expects the BOC to raise rates a couple times this year.

Thursday, February 17, 2011

Afternoon Market Video Update

Ashraf Laidi touches on the latest MidEast tensions and charting EURJPY, EURUSD & SP500 relative to bond yields.

Central Bank Diversification Into Commodity Currencies Continues

As you can see from the chart, the AUD, NZD, and CAD are all up against the USD over the last 6 months. The fact that the commodity-linked currencies have solid fundamentals and higher interest rates is just a bonus. Read more about this topic here.

Morning Currency Wrap for Thursday February 17, 2011

Safe Haven Flows, But Confined To A Range - The CHF, Yen, and gold rose across the board amid speculation unrest will keep spreading in North Africa and the Middle East, boosting demand for the safest assets. Yesterday in Bahrain, riot police crackdown on protesters killing at three people, while tensions in the Middle East were reinforced by plans, which were later canceled, for two Iranian warships to sail through the Suez Canal. In the UK, the GBP strengthened after Bank of England policy maker Andrew Sentance said the bank should raise interest rates to boost the GBP as a means of curbing inflationary pressures. Sentance has been the loan hawk on the Monetary Policy Committee but his term is up in May and I'm sure they will replace him with a dove. As for Nordic currencies, the NOK and the SEK both weakened against the USD and Euro after each country's central bank looked less likely to increase interest rates after disappointing economic news. In Norway, GDP growth slowed in Q4 while in Sweden it was weaker than expected retail sales and an increase in the unemployed that lowered expectation of faster rate hikes. In the US today, higher than expect jobless claims and consumer price inflation added to pressure on the USD and ticked gold prices higher. In Canada, the CAD continued its upward trajectory on firmer oil price and a positive outlook for global equity markets. The market is waiting to take its cue from Friday’s core inflation data which will shed light on any future Bank of Canada interest rate movement. The central bank makes its next announcement on interest rates on March 1.

Wednesday, February 16, 2011

Lagarde Talks Currencies Before G-20 Meet

French finance minister Christine Lagarde discussed plans to define indicators of global imbalances and the inclusion of the yuan in the basket of currencies making up the IMF's alternative reserve currency the Special Drawing Rights.

Morning Currency Wrap for Wednesday February 16, 2011

Sterling Gets Smacked With Stagflation On UK's Horizon - The GBP, which has been the best-performing currency so far this year due to growing speculation that the Bank of England would raise interest rates to fight inflationary pressure in the UK economy, was knocked down after the BOE dampened hawkish interest rate expectations. The BOE pared back its 2011 growth outlook that it had issued in November and raised its inflation outlook, which in my book spells stagflation. In fact, the BOE said that inflation will quicken from a two-year high and peak at about 4.4% before easing to its 2% target by the middle of 2012. Thus, the BOE may need to keep borrowing costs at a record low to aid a recovery that is “unlikely to be smooth.” Elsewhere, the CHF was down after the Swiss government announced steps to deal with a strong currency by providing support to exporters. I think the market misunderstood the Swiss government because all it did was announce measures to help businesses cope with the strong CHF not measures to curb CHF strength, so this is a buy the dip moment. In fact, the Swiss government said that any monetary steps were the responsibility of the Swiss National Bank and SNB Vice-President Philipp Hildebrand hinted that CHF strength would help to restrain inflation. Meanwhile, the Euro remained in a tight trading range against the USD and will probably remain that way until we get closer to the Irish election, where opposition parties have been making noise about renegotiating the EU/IMF bailout terms. In Asia, the Yen continued its decline as the risk trade continues as global recovery is gaining momentum. In Canada, the CAD was little change and remained in a tight trading range despite a disappointing read on the manufacturing sector. Statistics Canada reported that manufacturing sales were up by 0.4% in December, far less than the expected rise of 2.1 %. The market is waiting to take its cue from Friday’s core inflation data which will shed light on any future Bank of Canada interest rate movement.

Tuesday, February 15, 2011

Afternoon Market Video Update

Michael Hewson of CMC looks back at China CPI and UK CPI as well as ahead to Bank of England Inflation report, UK Unemployment, UK retail sales, US FOMC minutes, US retail sales, US weekly jobless. He also looks at GBPUSD, EURGBP and GBPJPY key chart levels.

Euroview: Euro's ECB Nightmare

Weber's retirement from the race to replace Trichet suggests his successor will be a less hawkish second-rate candidate, who will emerge amid debt-crisis horse-trading.

Morning Currency Wrap for Tuesday February 15, 2011

The Euro Fade & King's Letter #5 - The Euro moved up against the USD after German investor confidence increased this month but gains were capped due to persistent negative sentiment towards the Euro. The German ZEW index, which aims to predict developments six months in advance, increased to 15.7, from 15.4 in January, its fourth monthly gain. However, the Euro continues to be weighed down by upcoming elections in Ireland and parts of Germany, Portuguese bond yields over the magic number of 7% (which was the yield that Ireland and Greece had to throw in the towel), the lack of a comprehensive plan to tackle the sovereign debt crisis, and uncertainty over the next ECB president. I continue to recommend that any Euro rally should be shorted. In the UK, the GBP rose after U.K. consumer prices rose to the highest since November 2008. UK CPI rose to 4% in January, in line with economists' forecasts, from 3.7% in December. The implied yield on the short-sterling futures contract expiring in December increased 0.04 percentage point to 1.75% as traders increased bets that the Bank of England will boost interest rates. BOE Governor Mervyn King will now be forced to write letter #5 to the government explaining what remedial action will be taken. In Asia, China's inflation data came is softer than expected easing concerns that the world's No 2 economy will have to tighten monetary policy more aggressively. This has helped fuel the risk trade rally. In the US, the USD extended its losses against the Euro and trimmed its gains against the Yen after US retail sales rose less than expected. The Advance Retail Sales report for January showed a 0.3% increase in overall retail sales against an expectation of 0.5%. Also, figures for the prior month were revised downward. In Canada, the CAD continued to crawl higher within a tight range as firmer oil prices and the continued rally in the risk on trade.

Monday, February 14, 2011

US budget battle looms

The US economy is the world's largest, despite staggering public debt. President Barack Obama is expected to announce major budget cuts on Monday. But already, Republicans say those cuts won't go far enough. Al Jazeera speaks to Ashraf Laidi, an investment strategist for brokerage firm CMC Markets, in London - on the upcoming budget battle.

Euroview: Euro Jitters To Start The Week

The euro has started the week under a little pressure, but, with a data avalanche to come, it's not likely to remain in the unwelcome spotlight much longer.

Saturday, February 12, 2011

The Week Ahead by MarketWatch Videos

Asia's Week Ahead: Japan Economy; China Inflation

Feb. 11, 2011

Japan's quarterly economic data, China's monthly inflation figures and BHP Billiton's interim results will likely take center stage in Asia over the coming week. MarketWatch's Phani Kumar reports.

Europe's Week Ahead: Mobile World Congress

Feb. 12, 2011

Companies such as Samsung and Sony Ericsson will unveil new products at Mobile World Congress in Barcelona next week. Meanwhile, Barclays, Danone and Nestle are due to report earnings.

U.S. Week Ahead: Watching Egypt, Retail Data, Dell

Feb. 11, 2011

U.S. stocks head into the new week on a positive footing, a trend that could be affected in coming days by data on retail sales, earnings news from the likes of Dell and CBS, along with further developments in Egypt's political upheaval. Lauren Rudser reports from San Francisco.

Feb. 11, 2011

Japan's quarterly economic data, China's monthly inflation figures and BHP Billiton's interim results will likely take center stage in Asia over the coming week. MarketWatch's Phani Kumar reports.

Europe's Week Ahead: Mobile World Congress

Feb. 12, 2011

Companies such as Samsung and Sony Ericsson will unveil new products at Mobile World Congress in Barcelona next week. Meanwhile, Barclays, Danone and Nestle are due to report earnings.

U.S. Week Ahead: Watching Egypt, Retail Data, Dell

Feb. 11, 2011

U.S. stocks head into the new week on a positive footing, a trend that could be affected in coming days by data on retail sales, earnings news from the likes of Dell and CBS, along with further developments in Egypt's political upheaval. Lauren Rudser reports from San Francisco.

Friday, February 11, 2011

Morning Currency Wrap for Friday February 11, 2011

Instability In Egypt Causes Jittery Markets & Safe Haven Flows - As the crowd gathered in Cairo’s Tahrir Square, Egyptian President Hosni Mubarak said that he would delegate some powers to his vice president, but he refused to step down until September. This is not what the crowd wanted to hear, simply changing cronies is not going to cut it. The situation is getting tenser and that is being reflected in the markets as USD and gold are benefiting from safe haven flows. In Europe, the Euro continues to be weighed down by upcoming elections in Ireland and parts of Germany, Portuguese bond yields over the magic number of 7%, the lack of a comprehensive plan to tackle the sovereign debt crisis, and uncertainty over the next ECB president. The foot dragging you are witnessing here is mainly due to the elections in Germany - everyone knows what needs to be done here but they don't want to announce that Germany is prepared to raise the ante in fear that it could cause German Chancellor Angela Merkel to lose the support she needs to authorize it. In Asia, the AUD fell below par against the USD after Reserve Bank of Australia Governor Glenn Stevens told parliament that it was reasonable to expect rates to be on hold for some time. Meanwhile, the USD continued its climb against the Yen as bond yields continue to favor the US. In Canada, the CAD has bucked the trend and moved higher against the USD as December's trade data shows that Canada's trade balance returned to a surplus after nine months of deficits, fueling hopes the much-coveted export recovery is finally gaining traction. Also, firmer oil prices due to the turmoil in Egypt and the fear that the upheaval could spread to other countries in the oil-rich region are supporting the CAD.

Thursday, February 10, 2011

GBP Steady As U.K. Rates Left Unchanged

Speculation over an early U.K. rate hike will remain, helping the pound, unless it is ruled out by the Bank of England, or by new data, next week.

Morning Currency Wrap for Thursday February 10, 2011

Stocks Look Tired, Sovereign Debt Issue Weighs - The USD rose against all of its most-traded counterparts as global stock markets were down; and the US stock market has been rising only on fumes this week as the lack of volume on the way up is a red flag that the stock market is in need of a pause or correction. What will be very interesting is what will market players do in response to the correction. Could they shun stocks and bonds at the same time and go into commodities and precious metals? We are going to find out. Meanwhile, the Euro was down as the market is starting to get nervous about the lack of a concrete plan to tackle the European sovereign debt crisis, especially with the national elections in Ireland coming up. There is a real threat that the Irish people will demand better terms on their bailout or worse, that they will do what Iceland did and just default on all of their debts. It is not lost on the Irish public that Iceland is now flourishing after walking away from their debts. If Ireland were to take this road then there would be a lot of downward pressure on both the Euro and the GBP due to the exposure of European and UK banks - so expect a trading range until the election. Also weighing on the Euro was the fact that 10-year Portuguese bond yields hit an all-time high, widening the spread over its safe-haven German equivalent. The 10-year interest rate on Portuguese bonds hit 7.6%, not far off the level that forced Ireland to agree to a bailout, before falling back to 7.3% amid unconfirmed reports the ECB was buying the bonds to halt the rise. Elsewhere, the GBP slipped after the BOE’s Monetary Policy Committee left its bond program at 200 billion pounds ($321 billion) and kept the benchmark interest rate at a record low 0.5 %. There was a slight chance of an increase in rates but that didn't materialize. In Asia, the AUD was down after a report showed full-time employment dropped in January, fueling speculation the economy is growing too slowly to prompt the central bank to raise interest rates. While overall employment climbed by 24,000 jobs, full-time employment fell by 8,000. In Canada, the CAD was off its worst levels but remained range bound supported on news that Canada’s new home price index rose for a fifth month and U.S. first-time claims for unemployment insurance fell to the lowest level since July 2008.

Wednesday, February 9, 2011

Bernanke, Confidence Man or Con Man

In today's testimoney to the House Budget Committee, Federal Reserve Chairman Ben Bernanke told congress that rising bond yields are a result of investors' stronger confidence in the economic recovery, not worries about inflation. Really, every time I look at the chart below all I can think of is inflation. You be the judge.

Euroview: Euro Hit By Weber Talk

The euro was hit by talk that inflation hawk Axel Weber won't take the top job at the ECB after all, trimming rate-hike expectations. But it's a confusing situation, and the significance is open to question.

Morning Currency Wrap for Wednesday February 9, 2011

ECB Wants A Dove Not A Hawk? - The Euro has been able to recapture all of its initial losses on news that Bundesbank head Axel Weber may not be a candidate to replace Jean-Claude Trichet as President of the European Central Bank. Apparently, Weber mentioned in a private meeting on Tuesday that he may not want another term as Bundesbank president after his term expires in April 2012. Thus, European officials have interpreted the comment, along with other private conversations in which Mr. Weber has cast doubt on his future as a central banker, as a sign that he may not seek the ECB presidency. Weber, who had been considered a front-runner to succeed Trichet when his term expires in October, is regarded as a hawk on inflation but often finds himself in the minority. I guess they are looking for a dove like Bernanke, OMG. Elsewhere, the NZD was down across the board after Finance Minister Bill English said it was “possible” the economy slipped into recession in the second half of last year. The economy may have contracted in the fourth quarter of 2010, entering its second recession in two years, he said. Nothing is official yet but it sounds like English is trying to talk down the NZD or at least stop it from rising too much. In Japan, the USD was up against the Yen as yield differentials have moved in the USD's favor, especially against the Yen. The media will tell you that signs of a broadening US recovery and some hawkish commentary from Fed officials have contributed to higher US bond yields, but the truth is that the bond vigilantes have inflation on their radar and have sold off US bonds causing yields to rise. The market will focus on Chairman Ben Bernanke's testimony at 1500 GMT to the House Budget Committee and tomorrow's Bank of England policy meeting for direction. In Canada, the CAD was little changed from yesterday's close after loosing about a cent against the USD in yesterday's trading action on news that as oil prices were undermined by news that Suez Canal operations were unaffected by strikes, calming concerns about Mideast supplies.

Tuesday, February 8, 2011

The Fed's Role In Recent Inflation

Dylan Ratigan and Bill Fleckenstein explain the Fed's role in the recent rise in food prices around the world.

Visit msnbc.com for breaking news, world news, and news about the economy

Morning Currency Wrap for Tuesday February 8, 2011

First Of Four Chinese Rate Hikes - The Chinese interest rate hike finally came, it was expected before the start of the lunar holiday in Asia but may have been delayed due to development in Egypt. Chinese Inflation jumped to a 28-month high of 5.1% last November before moderating in December, but it has worried Chinese leaders who fear that a sharp rise in living costs could trigger unrest. The market has taken this in stride probably because it is the first of four that are expected this year - I don't think the risk trade will come off until we see a marked slow down in Chinese growth and production. As always, the first knee jerk reaction to the news was the AUD, which fell on speculation that growth in the world's No. 2 economy may slow. I suspect that the rate hike will weigh more on the AUD than the NZD or CAD due to deteriorating short-term economic data in Australia caused by the floods. Meanwhile, Asian market players, including sovereign names, continued to sell the USD since returning on Monday from the lunar new year holidays. With the risk trade on that means that the market will short the USD and the Yen. Euro sentiment was helped after ECB Governing Council member Yves Mersch argued on Monday that the central bank could raise rates before it ended measures to support liquidity. This statement helped the Euro after last week's comments by ECB President Jean-Claude Trichet doused expectations for an imminent interest rate rise. The rise in the Euro was temporarily capped after the second consecutive disappointing report out of Germany. This time around it was a steeper than expected 1.5% monthly drop in German industrial production in December, which was exacerbated by a 24.1% decline in construction activity amid harsh winter weather. Over in the UK, the GBP was under pressure after the U.K. increased a levy on bank balance sheets. U.K. Chancellor of the Exchequer George Osborne decided to implement the tax sooner than had been expected in order to raise an extra 800 million pounds ($1.3 billion) as he continues to negotiate lending targets and curbs on pay. In Canada, the CAD gave back its overnight gains after the rate hike in China to open little changed from yesterday's close.

Monday, February 7, 2011

UK Interest Rate Outlook

Chief Market Strategist at CMC Markets, Ashraf Laidi, comments on UK's interest rate decision this week.

Morning Currency Wrap for Monday February 7, 2011

USD Neutral After A Sharp Rise In US Interest Rates - That's right folks the market sets interest rates not the central banks. Central bank policy meetings are a side show filled with propaganda in order to give the illusion that they in control of the markets. Well the market has spoken, and the bond vigilantes have sold off long term US debt causing yields to rise because they see inflation on the horizon. Of course, nothing I read today even mentions this, all they talked about is how the USD was up due to the improvement in the US jobs market as evidenced by the fact that the unemployment rate went down to 9% from 9.4%. Bond vigilantes ignored the drop in the unemployment rate, as they should because it reflects the fact that people have given up looking for a job, and focused instead on the fact that average hourly earnings rose 0.4% from 0.1%, the fastest increase since Nov 2008. The combination of rising wages and runway food inflation in the rest of the world demonstrates the unfolding inflationary pressure that Bernanke just doesn't see or more like he doesn't want to admit to. Thus, rising US Treasury yields is putting a firm bid under the USD against the Euro and some of the other majors as sentiment switches from bearish to neutral on the USD - expect a trading range. Also, the Euro was weighed down by a larger-than-expected fall in German factory orders for December and by the lack of a concrete proposal coming out of the weekend's EU summit concerning the sovereign debt issue. Meanwhile, the GBP will probably trade sideways this week ahead of Thursday’s Bank of England meeting. No change is expected but the money market sees a one-in-five chance of a rate hike. In Asia, the Yen fell against the majors as the market expects interest rate rises every where except in Japan. In Canada, the CAD was firm against the USD and is trading in a tight range due to higher commodity prices and some positive economic data from the housing sector. Canadian building permits increased 2.4% to $5.7 billion in December, following two consecutive months of declines.

Saturday, February 5, 2011

The Week Ahead by MarketWatch Videos

Asia's Week Ahead: Results from Toyota, Nissan

Feb. 4, 2011

Earnings reports from Toyota, Nissan and Rio Tinto will be in the spotlight, as will core machinery orders from Japan and a rate decision from South Korea. MarketWatch's Lisa Twaronite reports.

Europe's Week Ahead: Swiss Banks In Focus

Feb. 4, 2011

Swiss banking giants UBS AG and Credit Suisse Group AG are due to report quarterly earnings next week. The Bank of England is expected to leave monetary policy unchanged.

U.S. Week Ahead: Markets at 2-Year Highs

Feb. 4, 2011

With the Dow and S&P above psychologically important levels, a lean slate of data along with earnings from insurers and REITs could propel stocks from their current perches. Greg Morcroft reports.

Feb. 4, 2011

Earnings reports from Toyota, Nissan and Rio Tinto will be in the spotlight, as will core machinery orders from Japan and a rate decision from South Korea. MarketWatch's Lisa Twaronite reports.

Europe's Week Ahead: Swiss Banks In Focus

Feb. 4, 2011

Swiss banking giants UBS AG and Credit Suisse Group AG are due to report quarterly earnings next week. The Bank of England is expected to leave monetary policy unchanged.

U.S. Week Ahead: Markets at 2-Year Highs

Feb. 4, 2011

With the Dow and S&P above psychologically important levels, a lean slate of data along with earnings from insurers and REITs could propel stocks from their current perches. Greg Morcroft reports.

Friday, February 4, 2011

Daily Market Update by Ashraf Laidi

Ashraf Laidi covers the US & Canada jobs report & the impact on GBPUSD, AUDUSD, Treasuries & Gold.

Morning Currency Wrap for Friday February 4, 2011

U.S. Job's Report Was Terrible, But USD Up Anyway - Nonfarm payrolls for January increased by 36K, which is a far cry from the increase of 148K that had been expected. Despite the smaller-than-expected increases, the headline unemployment rate fell sharply to 9.0% from 9.4% in December. But this is not good news because the drop in the unemployment rate is mostly due to discouraged workers leaving the labor force. After all, Fed Chairman Bernanke just stated yesterday that the economic recovery hasn't been strong enough to significantly reduce unemployment and that it will be several years before the unemployment rate returns to a more normal level. Surprising the USD was up against the Euro and the GBP despite the terrible jobs data. It looks like that European Central Bank President Jean-Claude Trichet's comments yesterday after the ECB policy meeting was able to dampen speculation on early interest rate increases. Trichet said inflation expectations remained firmly anchored and inflationary pressures over the medium to long term should remain contained, which prompted euro zone interest rate futures to pare expectations of a rate increase by August to around 90% after having fully priced one in beforehand. Also, weighing on the Euro was the return of the European sovereign debt crises to the front pages with today EU summit. Very few market players expect anything startling to emerge as measures to reinforce a bailout scheme for struggling member states are not expected to be taken until March. In Asia, the USD was up against the Yen as the recent rise in bond yields continues to favor the U.S. over Japan. Meanwhile, the USD was down against the dollar block currencies of the AUD, NZD, and CAD, which are showing better growth prospects and higher interest rate expectations that the U.S. An example of this was the performance of the CAD today, Canada added 69,200 more jobs in January, far more than most forecasts, while the unemployment rate unexpectedly ticked up from 7.6% to 7.8%. It was the fourth highest payroll number in the last five years and to put it perspective the 69K increase for Canada is the equivalent of about 600K increase in the US, Wow.

Thursday, February 3, 2011

Time to Bet on the Dollar?

As the dollar dives to 12-week lows, the euro's been rebounding, with Ashraf Laidi, CMC Markets, and Simon Derrick, BNY Mellon.

Morning Currency Wrap for Thursday February 3, 2011

Waiting On The Grey Haired Silver Foxes - The service sector for both the euro zone and the UK came in stronger than expected for the month of January. Euro zone PMI rose to 55.9 from December's reading of 54.2 while the UK PMI jumped to 54.5 form 49.7 and well above the 51.3 that was expected. Therefore, the strong reading in the service sector today coupled with the strength of the manufacturing PMI earlier in the week, reinforce the notion that the euro zone and the UK recovery are broadening. Today's data caused profit taking in the Euro because market players wanted to hear the press conference of silver fox #1, ECB President Jean-Claude Trichet after the ECB policy meeting today. The market want to see if he diverges from his recent warnings on the need to tackle inflationary pressures. Meanwhile, today's data for the UK caused the GBP to surge higher against the USD as the data boosted speculation that the Bank of England has room to raise interest rates this year. The GBP did not sell off like the Euro did because silver fox #2, Bank of England Governor Mervyn King, doesn't need to speak until next week's policy meeting. As for silver fox #3, U.S. Federal Reserve Chairman Ben Bernanke, is due to speak at 12:30 EST, where he will reaffirm the Fed's focus on boosting growth and employment. In Asia, the AUD was up against the USD after strong Australian trade data and domestic building permits adding to signs that the economy remains resilience despite vast flooding and cyclones. Remember trading activity is quieter than usual amid Asian markets which remained closed for the Lunar New Year holiday. In Canada, the CAD was little changed against the USD after hitting a its strongest level in two weeks. The market is awaiting tomorrow's employment report for both the U.S. and Canada. Keep in mind that anything that indicates that U.S. growth is stronger than expected has been a positive for the Canadian growth outlook and the CAD.

Wednesday, February 2, 2011

AUD, CAD, and Commodity Prices

Morning Currency Wrap for Wednesday February 2, 2011

QE3 & The Price Of Rice - After observing what has been transpiring in Northern Africa and Egypt over the escalating price of food, especially the grains, I decided to see what the price of the world's most popular food was doing. Well this week the price of rice is only up over 7%, and it is at its highest price in the last twelve month period. Yesterday came news from Kansas City Fed President Thomas Hoenig that the Fed could debate extending its bond-buying program beyond June if U.S. economic data proves weaker than expected. Well I think if QE3 becomes a reality then it will be the last nail in the coffin for the USD. FYI to China, if you think that the price of rice is high now I can assure you that QE3 will cause the price to surge. Now back to the markets, the Euro gave back some of yesterday's gains after Ireland’s credit rating was cut by Standard & Poor’s. The downgrade was a reminder to the market that the European sovereign debt crises is still with us, but the market is also aware that EU leaders have been signaling that they are working on a comprehensive plan to tackle the issue - so expect only a temporary loss of momentum for the Euro. In fact, recent public opinion is saying that Europeans want Germany to take more control which is giving Germany the green light to extract measures in exchange for more money. Elsewhere, the GBP has rallied to a three-month high against the USD after a report showed the U.K. construction sector returned to growth, increasing the market's confidence that the BOE will hike rates. In Asia, most Asian currencies moved higher on signs of improved global growth while the Yen remained in a tight range against the USD. The key driver in the forex market right now is the perception that the U.S. Federal Reserve will continue with its easy monetary policy while the rest of the world continues to raise interest rates or is in the process of moving to interest hikes later in the year. Hoenig admission yesterday about QE3 only reinforces this perception. Also, the USD as lost it safe haven appeal as the market discounts the situation in Egypt as merely a political event. In Canada, the CAD was higher in overnight trading as recent global data points to a global economic recovery that is gaining traction. The key data for Canada this week will be the employment numbers on Friday for both Canada and the U.S.

Tuesday, February 1, 2011

Carney Says Canadian Dollar `Strength' Threatens Growth

Morning Currency Wrap for Tuesday February 1, 2011

Higher Growth & Interest Rate Expectations Everywhere, Except U.S. - A strong round of economic data from the euro zone and the UK, along with higher interest rate expectations caused market players to abandon safe haven flows due to turmoil in Northern Africa and Egypt. The situation in Egypt has not been resolved as President Mubarak’s refusal to cede control of power illustrates, but for the moment they have not escalated - so traders have trimmed their risk aversion bets. Euro zone factory activity accelerated at its fastest pace in nine months as the Markit PAM unexpectedly jumped in January. Growth was led by Germany, but the data also showed signs of activity picking up in peripheral nations. More importantly, the PAM surveys also showed rising price pressures, adding to expectations that European Central Bank President Jean-Claude Trichet will keep a hawkish tone on Thursday. In fact, interest rate futures suggest a nearly 80% possibility the ECB will raise rates by 25 basis points in August from the current record low of 1%. Also, German unemployment showed a seasonally adjusted decline of 13,000 in January, which was greater than expected. All of this news has helped the Euro rally o its highest level against the USD in more than two months. In the UK, the GBP rallied to 2-1/2 month high against the USD after U.K. manufacturing PAM jumped to a record 62.0 for January. Also powering the GBP higher was news that the National Institute of Economic and Social Research suggested that the Bank of England will raise its key interest rate three times this year to prevent a surge in consumer prices from getting entrenched in the economy. In Asia, the AUD jumped over parity versus the USD after the Australian central bank ended its monthly policy meeting with a generally upbeat assessment of the domestic and global economy, signaling that higher interest rates could be ahead. So there you have it - a contrast of higher growth and interest rate expectations versus the expectation that the US Fed will leave rates on hold for at least another year and half. In Canada, the CAD slipped back up over parity against a broadly softer USD. Yesterday, the CAD had lost almost a penny after Finance Minister Jim Flaherty's cautious remarks on employment prompted investors to price in a weak January jobs figure on Friday.

Subscribe to:

Comments (Atom)